The Latest Insights and Analysis from Chris Cui, Director of Asia Programs

November 18, 2019

Chris shares her latest thoughts and takeaways from a recent trip to China where she attended the 14th China International Plastics Recycling Conference & Exhibition and visited a local MRF.

China’s Material Recovery Facilities Are Fast Adapting To A Post National Sword World

We gained valuable market insights from policy makers and market practitioners at the 14th China International Plastics Recycling Conference & Exhibition in September in Shanghai. The discussion focused on how stakeholders across the recycling system should work together to develop a domestic closed-loop ecosystem. This means doubling down on collection, transportation, and reprocessing efforts to enable brands to reach their circularity goals. It became clear that the Chinese government is determined and committed to supporting the development of the circular economy in the coming years by carrying out the following policies:

- Implementing a tax to support the recycling industry

- Creating green standards for recycled plastic and for the production of recycled plastic

We saw firsthand the rationale behind these policies that are being considered. Mr. Wang, the Secretary of CRRA, was also quick to note the number of new faces in the room, including brand owners and capital providers, like Closed Loop Partners and the Alliance to End Plastic Waste. This helped to send a strong signal to the recycling industry around the business case for the circular economy.

Chris promoting the circular economy to brand owners & the recycling industry in China, Shanghai.

Witnessing The Transformation Of A Traditional MRF Into A Tech Enhanced One

It’s been three months since mandatory trash sorting was enforced in Shanghai and other big cities across China. We visited a local MRF to see how the new laws have impacted business. Tianqiang, led by CEO Mrs. Hu, has transformed its business model from a MRF to an all encompassing solutions provider, adding collection, reprocessing and production capacity.

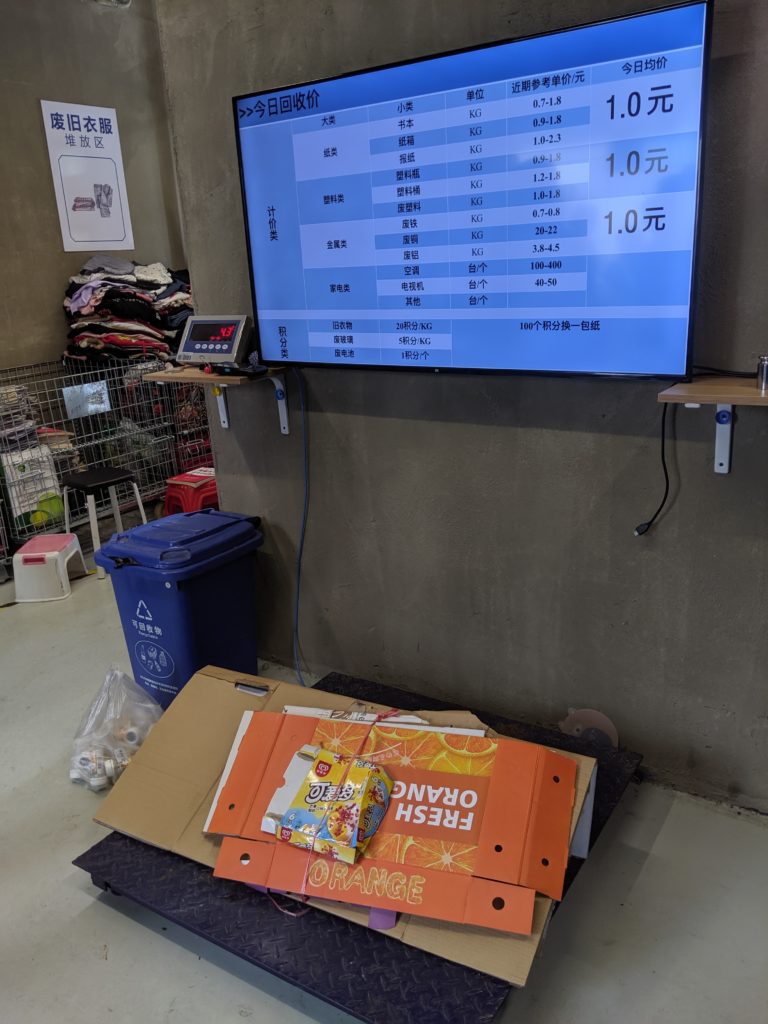

- Tianqiang has implemented technology enabled collection services. They have set up café style smart collection centers with digital scales that are linked to real time commodity prices. Residents get paid immediately by cash or credit according to the commodity price on a given day. Also, operators of the MRF are able to see the exact amount of recyclables collected from each transaction and accumulated at each center on a dashboard. This data helps inform the local government’s waste reduction targets for different communities.

Weighing paper recyclables at Tianqiang.

- Tianqiang is embracing vertical integration. Although their recycled plastic is sold mainly to car and furniture manufacturers, they are also producing their own products such as clothes hangers to sell to retailers. Their recycled paper is being sold directly to the no. 1 and no. 2 paper products manufacturers in China.

- Tianqiang’s collection centers are rent free, strengthening an earlier point that the Chinese government is supporting the development of local recycling infrastructure, for example by providing free land to encourage private sector growth.

Locals separating and sorting recyclables at Tianqiang.

Related posts

Press Release

Closed Loop Partners Backs Supersede’s Expansion...

The financing from Closed Loop Catalytic Capital &...

Press Release

Closed Loop Partners’ Private Equity Group Acquires...

The circular economy-focused investment firm’s acquisition...

Press Release

Public-Private Partnership with Providence Joins to...

Multi-million-dollar investment to provide high-capacity...

Blog Post

What It Takes to Build a Resilient Economy in 2026

Tazia Smith highlights major milestones for Closed...

Press Release

Closed Loop Center for the Circular Economy Launches...

The Closed Loop Center responds to composters’ increasing...

Press Release

Closed Loop Partners Deploys Multi-Million-Dollar Loan...

The catalytic loan from the circular economy-focused...

Press Release

Closed Loop Partners Releases New Guidelines to Strengthen...

The new guide shares tactical best practices to help...

Press Release

Closed Loop Partners Deploys $10 Million Loan to TemperPack,...

This marks Closed Loop Catalytic Capital & Private...

Press Release

Closed Loop Partners’ Composting Consortium, With...

Eight municipal and composter-led projects received...

Blog Post

Materials Matter: Designing Reuse for the Real World

One of the most important design decisions for reuse...

Press Release

Closed Loop Partners Advances Major Progress for the...

The circular economy-focused firm releases 2024 impact...

Press Release

Beyond the Bag Initiative Unites Major and Local Retailers...

Headlined by Target, CVS Health, Ralphs and Food 4...