Research and analysis

A Landscape Mapping of the Molecular Plastics Recycling Market

Molecular recycling technologies can contribute one piece to the puzzle, solving for our hardest-to-recycle plastic-based products, such as healthcare-related plastics, multi-layer packaging, apparel and building materials

In April 2019, we produced a first-of-its-kind report on Accelerating Circular Supply Chains for Plastics: A Landscape of Transformational Technologies that Stop Plastic Waste, Keep Materials in Play and Grow Markets. This defined the scope and landscape of technologies that could significantly advance the transformation of post-consumer plastics into the building blocks for new materials and countless end uses.

This report is part of Closed Loop Partners’ Advancing Circular Systems for Plastics & Packaging to accelerate solutions that enable circular systems for plastics. Building on the insights gained through our research, the next phase of work will create an Investor and Partnership Roadmap to further demystify the diverse technologies and their economic, environmental and human health impacts –– in addition to the incentives and policies that will support and ensure the sector finds an optimal place within the circular economy. We will continue to educate and explore in this space as the field develops.

Key Findings

TECHNOLOGIES THAT KEEP PLASTICS IN PLAY MUST BE PART OF THE SOLUTION TO END PLASTICS POLLUTION.

- Demand for plastics is strong and growing, yet the supply of recycled plastics available to meet demand is stuck at 6%.

- There are an estimated 34+ million metric tons of plastics landfilled or incinerated in the US and Canada each year.

- Current infrastructure and technology are limited in transforming all of the diverse types of plastics we use today into high-value feedstocks that compete with prime, or virgin, materials.

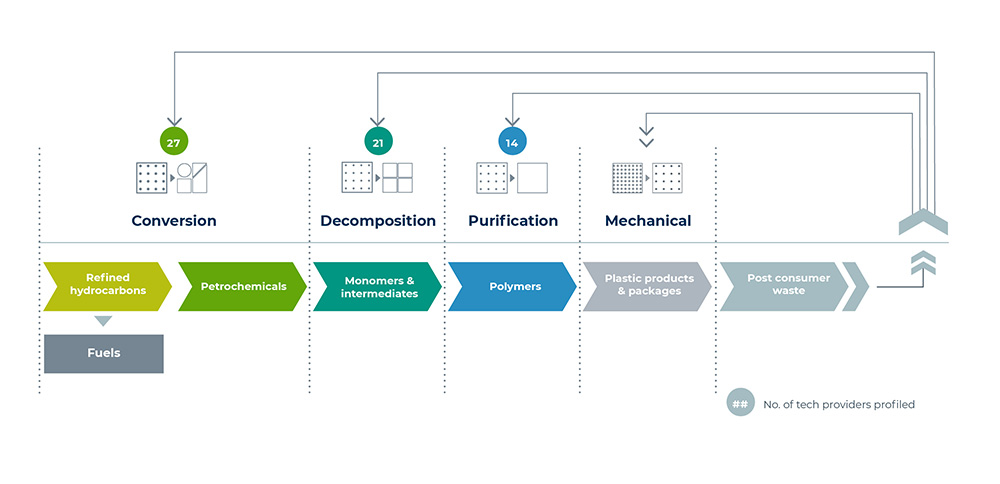

- Technologies exist to repurpose these plastics into valuable materials; purification, depolymerization, and conversion technologies can all play a role

THERE IS REAL DEMAND FOR PLASTICS AND OTHER MATERIALS ACROSS THE SUPPLY CHAIN.

THERE IS REAL DEMAND FOR PLASTICS AND OTHER MATERIALS ACROSS THE SUPPLY CHAIN.

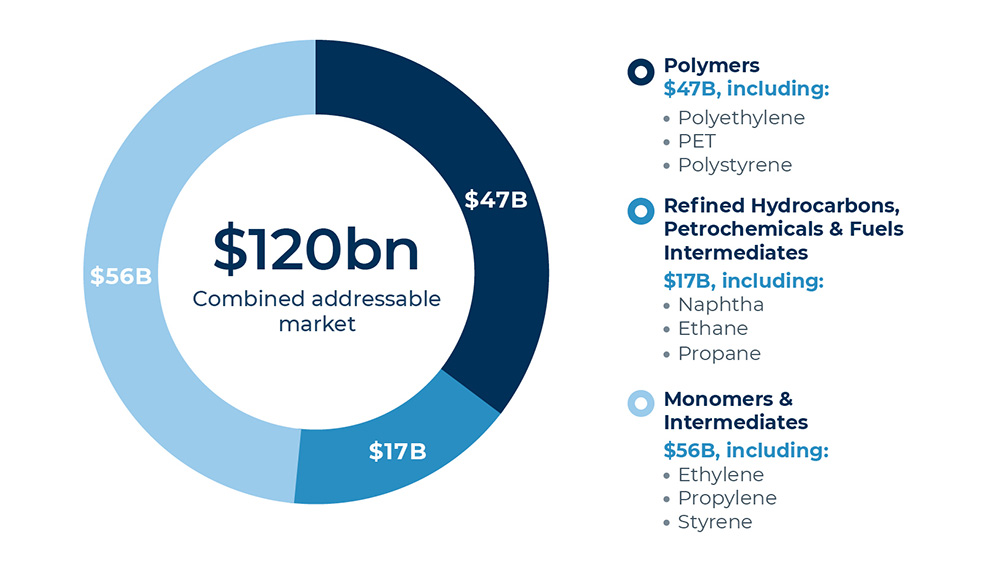

- Our analysis indicates that these technologies could meet an addressable market with potential revenue opportunities of $120 billion in US and Canada alone.

- The world’s largest brands, retailers and plastics manufacturers are making commitments around plastics recycling, recycled and recyclable content, and recovery. Current projections indicate new demand of 5 to 7.5 million metric tons by 2030.

- Beyond plastics, the demand also exists for chemicals and fuels – creating even more opportunity for waste plastics to be repurposed into materials that can continue to flow through our economy.

THIS IS POSSIBLE. THE INNOVATION EXISTS TO MEET THE DEMAND.

- 60 technology providers, nearly all of them at least at the lab stage of maturity, with significant potential to grow and scale (see map below). More than 40 technology providers are operating commercial scale plants in the U.S. and Canada today, or have plans to do so in the next two years.

- There is money to be made. Technology providers are operating profitably with higher margins as they mature and scale.

- 250 investors and strategic partners, including the world’s largest brands, private investors, petrochemical companies and plastic manufacturers, and government and NGO partners, are already engaging with the companies profiled in the report.

- Going from “possible” to “probable” will require: new solutions and business models that integrate innovations with existing infrastructure, flexible technology platforms that can evolve over time, and market incentives driven by public and private policies.

Interactive Data

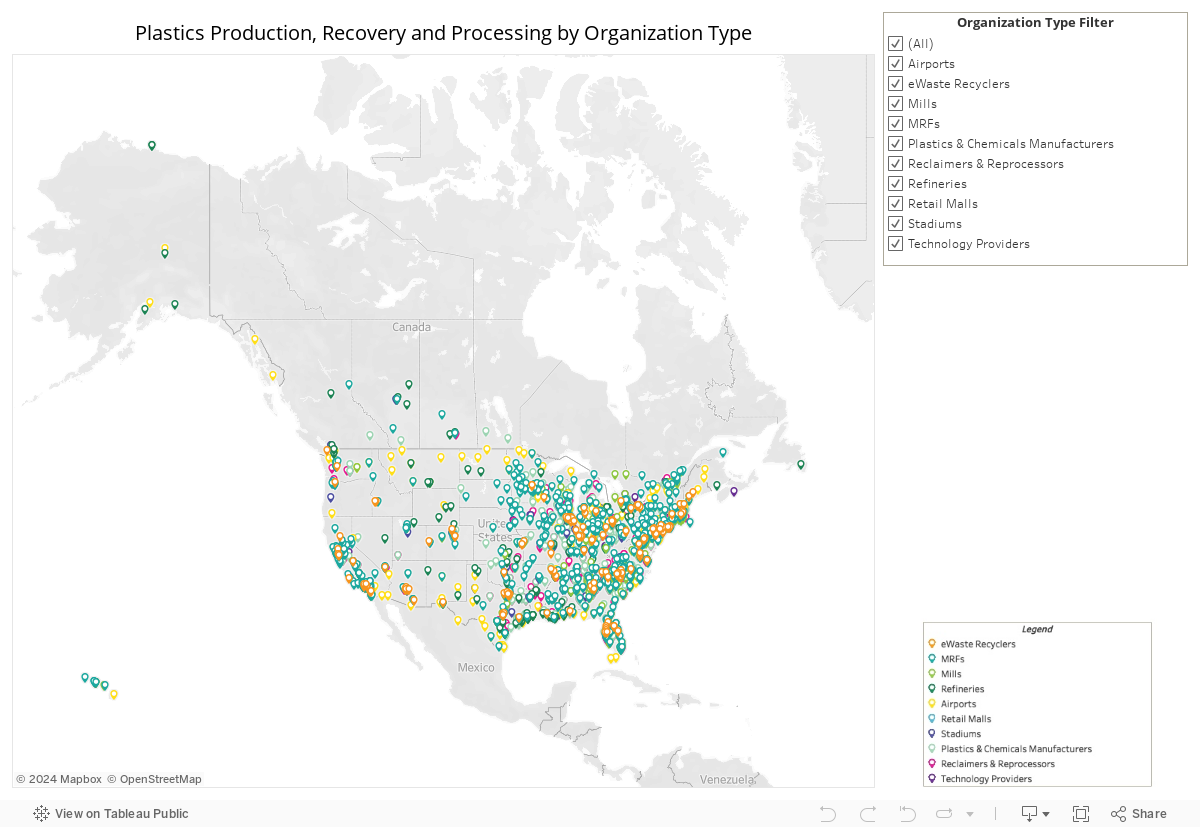

Plastics Production, Recovery and Processing by Organization Type

Data only available in desktop view.

Media coverage

Peter Makey

Press Release

Closed Loop Partners Backs Supersede’s Expansion…

The financing from Closed Loop Catalytic Capital &…

Press Release

Closed Loop Partners’ Private Equity Group Acquires…

The circular economy-focused investment firm’s acquisition…

Press Release

Public-Private Partnership with Providence Joins to…

Multi-million-dollar investment to provide high-capacity…

Blog Post

What It Takes to Build a Resilient Economy in 2026

Tazia Smith highlights major milestones for Closed…

Press Release

Closed Loop Center for the Circular Economy Launches…

The Closed Loop Center responds to composters’ increasing…

Press Release

Closed Loop Partners Deploys Multi-Million-Dollar Loan…

The catalytic loan from the circular economy-focused…

Press Release

Closed Loop Partners Releases New Guidelines to Strengthen…

The new guide shares tactical best practices to help…

Research

Best Practices for Future-Proofing Recycling Operations:…

The new guide shares tactical best practices to help…

Blog Post

What Did It Take for Austin, Texas to Start Recycling…

The NextGen Consortium interviews Circular Services…

Press Release

Closed Loop Partners Deploys $10 Million Loan to TemperPack,…

This marks Closed Loop Catalytic Capital & Private…

Press Release

Closed Loop Partners’ Composting Consortium, With…

Eight municipal and composter-led projects received…

If you are interested in participating in our ongoing research, convening and investment in this area, we encourage you to introduce yourself to the Center for the Circular Economy: [email protected]

Closed Loop Partners would like to thank the following individuals and organizations for their contributions and advice: AFARA, American Chemistry Council, Association of Plastics Recyclers, Earnscliffe Group, Gangadhar Jogikalmath, Google, GreenBlue, IHS Markit, Manteis Development Group and the Sustainable Packaging Coalition.

Graphic Design & Illustrations By: Anna Engstrom Studio LLC

Media coverage

GreenBiz

The 5 things you need to know about chemical recycling

Waste 360

Closed Loop Unveils New Report: “Accelerating…

Plastics News

Study: Chemical recycling development ‘not fast…

WasteDive

Closed Loop report calls for increased investment in…

Plastics Technology

New Closed Loop Study Takes Closer Look At Innovative…

Resource Recycling

Study details ‘transformational’ tech in plastics…

Recycling Today

Keeping plastics in play

Fast Company

Are we on the brink of a recycling revolution?

Bloomberg

These Companies Are Trying to Reinvent Recycling